Trust-Rails: The Checkless Rollover Solution

Modernizing how retirement assets move between custodians — digitally, instantly, and with full accountability.

We Built This Because We Lived It

The participant's side of the story

Between the two of us, we've changed jobs more than a dozen times. Different industries, different cities, different stages of life. But every single time, the same gut-wrenching experience: rolling over a 401(k).

One of us had it happen during the Great Recession — watching a retirement check sit on the kitchen counter while the market swung wildly, powerless to do anything but wait. The other went through it at the worst possible time, right before a major market dip, only to watch the money sit in limbo for weeks while better prices came and went.

We've filled out the same redundant forms, made the same frustrating phone calls, and felt the same knot in our stomachs when a check carrying our entire financial future showed up at the house.

Every time, we asked the same question: Why is this still how it works?

We each hold an MBA, with decades of experience in software product management. We know the Rule of 72.² We know that every 1% in fees compounds into devastating losses over a career. We've personally watched hidden fees silently destroy returns — turning what should have doubled into something far less. And we know that the technology to fix this has existed for years. It just hasn't been applied to this problem.

50 years of progress. Same process.

The Other Side of the Same Problem

The custodian's side of the story

While participants anxiously wait for checks, custodians are fighting their own battle. Plan administrators process stacks of paper forms by hand. Compliance officers worry about fiduciary liability every time retirement assets disappear into the postal system. Support teams field the same call dozens of times a day: "Where is my money?"

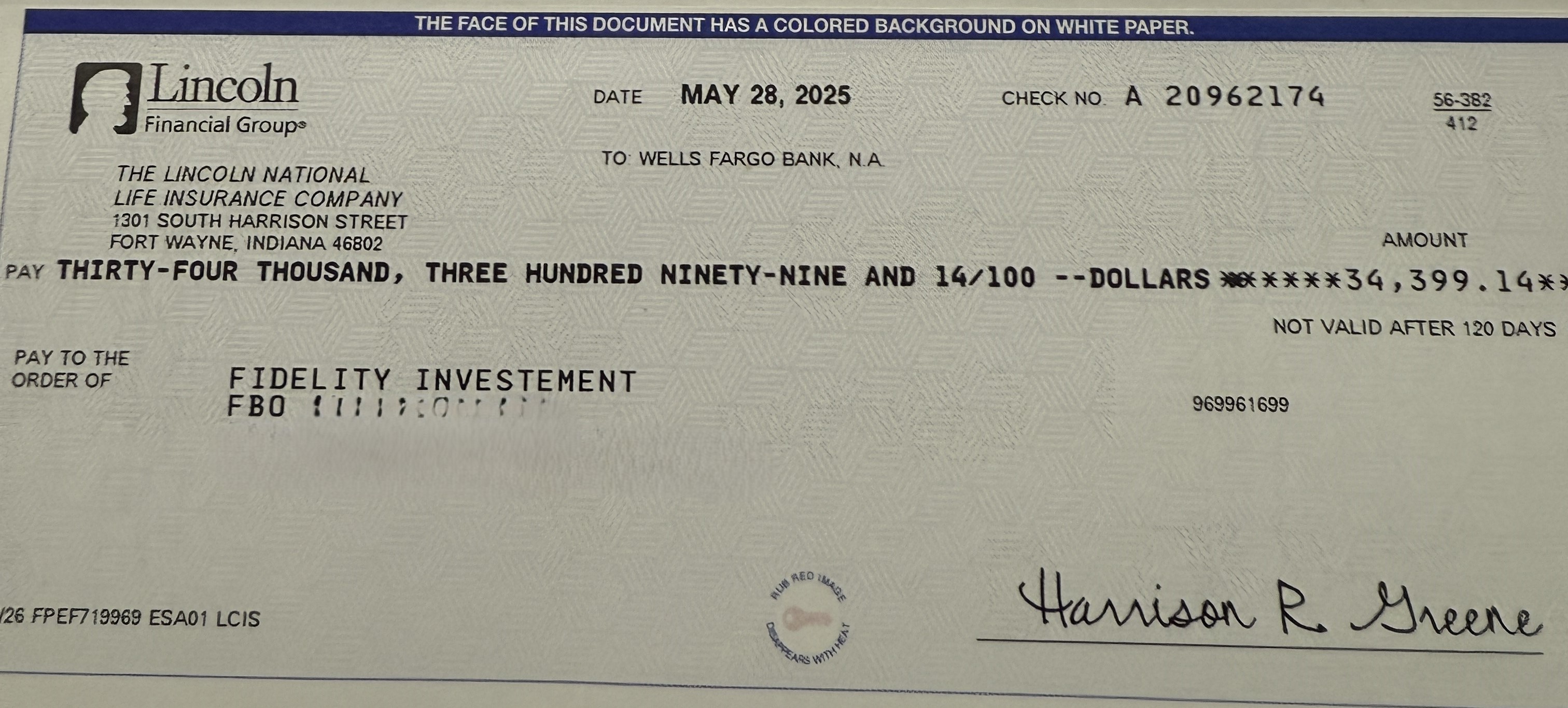

And then there's the fraud. Check fraud in the US has exploded — FinCEN reported that suspicious activity reports related to check fraud nearly doubled between 2021 and 2023⁹. Mail theft rings now specifically target retirement checks because they carry five- and six-figure balances with predictable timing. A participant changes jobs, a check gets cut, and somewhere between the sending custodian's mailroom and the participant's kitchen counter, it becomes a target. Checks get stolen from mailboxes, washed, and rewritten. By the time anyone notices, the money is gone — and the lawsuits aren't far behind.

Sending custodians have no way to confirm that funds arrived safely at the receiving institution. Receiving custodians have no visibility into when — or if — a transfer is coming. Both sides are operating blind, stitching together phone calls, faxes, and emails to track assets that could be worth a lifetime of savings.

The result? Lost AUM as frustrated participants cash out instead of rolling over. Mounting fraud exposure with every check that enters the postal system. Compliance risk that grows with every untracked transfer. And a process that makes custodians look like they're stuck in the past — because they are.

Fraud Exposure

Paper checks are the #1 target for mail theft and check washing — retirement checks carry six-figure balances

Fiduciary Risk

A stolen or lost check turns into an ERISA liability — and participants hold the plan sponsor responsible

Zero Visibility

Neither sending nor receiving custodian can see the transfer status in real time — fraud goes undetected for weeks

The Cost of Doing Nothing

The rollover process is so broken that roughly 40% of workers who leave a job simply cash out their 401(k) instead of rolling it over⁴. The result: an estimated $92 billion in annual savings leakage from taxes, penalties, and lost compounding⁵. The Employee Benefit Research Institute estimates the 401(k) ecosystem would hold nearly $2 trillion more if workers didn't cash out at job changes.

For those who do roll over, the process still punishes them. Check-based transfers take 30+ days⁶, during which $855 billion in annual rollover volume sits completely out of the market⁷. As JP Morgan's 2026 Guide to Retirement shows, missing just 10 of the market's best days over 20 years cuts your annualized return by nearly half³. Seven of those best days occurred within two weeks of the worst days — meaning the recovery participants miss while waiting for a check to clear is often the most valuable.

Then there are the accounts that simply get left behind. As of 2025, Americans had forgotten about 31.9 million retirement accounts holding an estimated $2.1 trillion in forgotten assets⁸ — money that's not growing, not consolidated, and not working for anyone.

American families lose hundreds of billions of dollars to a rollover process that drives cash-outs, market losses, and forgotten savings.

The Real Cost of a Broken Rollover Process

Where These Stories Meet

We've been on both sides of this problem — as participants watching our savings disappear into the mail, and as technologists who know that the infrastructure to fix it already exists. We built TrustRails to be the coordination layer that connects both sides of every rollover: participants who deserve visibility, and custodians who need control.

TrustRails gives every party — sender, receiver, and participant — a shared, real-time view of the transfer from start to finish. Funds move digitally between custodians in hours, not weeks. Every step is tracked, verified, and visible. No checks in the mail. No money in limbo. No one left guessing.

We're a technology layer, not a custodian. We never touch, hold, or take custody of participant funds. Your sending and receiving custodians maintain full control of all assets throughout the process — TrustRails provides the infrastructure that lets them coordinate securely and transparently.

We're not just digitizing the old process. You can wire six figures across borders in minutes, settle stock trades in a single day, and move money between bank accounts with a tap — yet rolling over a 401(k) still requires paper forms, mailed checks, and weeks of waiting. We're closing that gap.

Washington has spent decades focused on getting people into retirement plans — auto-enrollment, auto-escalation, SECURE 2.0. But no one has fixed what happens when people change jobs and need to move their savings forward. Policy has been building a bigger bucket while ignoring the hole in the bottom. We're plugging that hole.

The checks stop here.

No More Checks

Fully digital transfers eliminate fraud exposure and lost mail

No More Delays

Hours, not weeks — participants stay invested through the transition

No More Guessing

Every party tracks every step in real time

References

- ¹ Investment Company Institute, "Quarterly Retirement Market Data" (Total US retirement assets totaled $49.1 trillion as of Q4 2025)

- ² Investopedia, "Rule of 72" (A method for estimating an investment's doubling time by dividing 72 by the interest rate)

- ³ JP Morgan Asset Management, "2026 Guide to Retirement" (Missing 10 best days over 20 years cuts annualized returns by nearly half; 7 of the 10 best days occurred within 2 weeks of the 10 worst days)

- ⁴ Employee Benefit Research Institute (EBRI) / Savings Preservation Working Group (Approximately 40% of workers cash out their 401(k) at job change; the 401(k) ecosystem would hold nearly $2 trillion more if workers didn't cash out)

- ⁵ RCH / 401k Specialist, "The Definitive Guide to 401(k) Cashout Leakage" (Estimated $92 billion in annual savings leakage from taxes, penalties, and lost compounding)

- ⁶ ADP, "401(k) Rollover Guide"; Carry, "How Long Does a 401k Rollover Take?" (Check-based rollovers routinely take 30+ days including mail and processing time)

- ⁷ LIMRA/NAPA, "Annual IRA Rollover Activity Projected to Exceed $1 Trillion by 2030" (2025 retail rollover volume: $855 billion, up from $612 billion in 2020; projected to reach $1.15 trillion by 2030)

- ⁸ Capitalize, "The True Cost of Forgotten 401(k) Accounts" (As of 2025, 31.9 million forgotten accounts holding an estimated $2.1 trillion in assets)

- ⁹ FinCEN, "Financial Trend Analysis: Check Fraud" (Suspicious activity reports related to check fraud nearly doubled from 2021 to 2023)

Ready to Move Forward?

See how TrustRails is replacing checks with instant, trackable retirement transfers.